Closing Line Value and Why It Matters More Than Your Win Rate

- The metric that exposed my own self-deception

- Why bookmakers care about the closing line

- The maths of why it matters

- How to actually measure CLV in practice

- Why early markets give the most CLV opportunity

- The trap of confusing line movement with CLV

- Markets where CLV is most reliable

- What CLV cannot tell you

- The honest accounting that changed my approach

The metric that exposed my own self-deception

For three seasons I thought I was a profitable NBA bettor. I had a winning record, a positive ROI on my own spreadsheet, and a comfortable feeling that I had figured something out. Then I started tracking closing line value seriously, and the numbers told me I had been getting lucky. My ROI was real for the period it covered. My edge was not. The difference is the entire reason CLV exists as a concept, and it is the most important thing any serious NBA bettor in the UK should be measuring.

Closing line value is the gap between the price you got on a bet and the price that bet was sitting at when the market closed. If you took the Lakers at +3.5 and the line closed at +2.5, you got a full point of value. That point is the signal. The win-loss outcome of the bet is noise.

Why bookmakers care about the closing line

The closing line of a major NBA market is the closest thing to a fair price the betting industry produces. It represents the aggregated opinion of every sharp bettor, every model, and every piece of late-breaking information funnelled into a single number minutes before tip-off. The books have spent billions of dollars over decades refining this estimate, and the closing line is the output of that investment.

If you can consistently beat that number, by definition you have information or analysis the aggregated market does not. That is the only durable edge in this sport. Anything else is a temporary mispricing that will get corrected, a soft market that will get sharpened, or pure variance.

This is why books restrict and ban accounts that show consistent CLV. They are not afraid of bettors who win. They are afraid of bettors who beat the close, because those are the bettors who will keep winning. The win-loss record might lie. CLV does not.

The maths of why it matters

Run a thought experiment. Two bettors place 1000 bets each over a season. Bettor A wins 53 percent and gets average odds of 1.95. Bettor B wins 51 percent at the same odds. On the surface, A is the better bettor. But suppose Bettor A’s bets averaged no CLV – they got the same number the market closed at. And suppose Bettor B’s bets averaged half a point of CLV across the spread market.

In a year, Bettor A’s edge evaporates as the market corrects whatever soft spots they were exploiting. Bettor B’s edge survives, because they were consistently identifying mispricing before the market corrected it. The 2 percent win-rate difference reverses within 18 months, because B was making good bets that happened to lose and A was making mediocre bets that happened to win.

I lived through exactly this scenario. The third season of my «winning» stretch ended at minus 8 percent ROI. Looking back, my CLV had been negative the entire time. The market was telling me I was wrong. I was just not listening.

How to actually measure CLV in practice

Track every bet you place with five columns: the bet, your stake, the price you took, the closing price, and the result. The closing price is the awkward one – most UK books do not display it after the market closes. You have two options: screenshot the line at tip-off and record manually, or use one of the line-history sites that captures market movements across multiple books.

For NBA spreads and totals, half a point of CLV averaged across your bets is meaningful. A full point is excellent. If you are getting more than that consistently, you should be sizing bigger because you have a real edge. If your CLV is negative – you are getting worse prices than the market closes at – you have a problem the win-loss record will mask for a while and then expose brutally.

Run this analysis monthly. Do not wait until the end of the season. Three bad months of negative CLV is enough signal to change your process. Waiting for the win-loss record to confirm the bad news costs you the rest of the season.

Why early markets give the most CLV opportunity

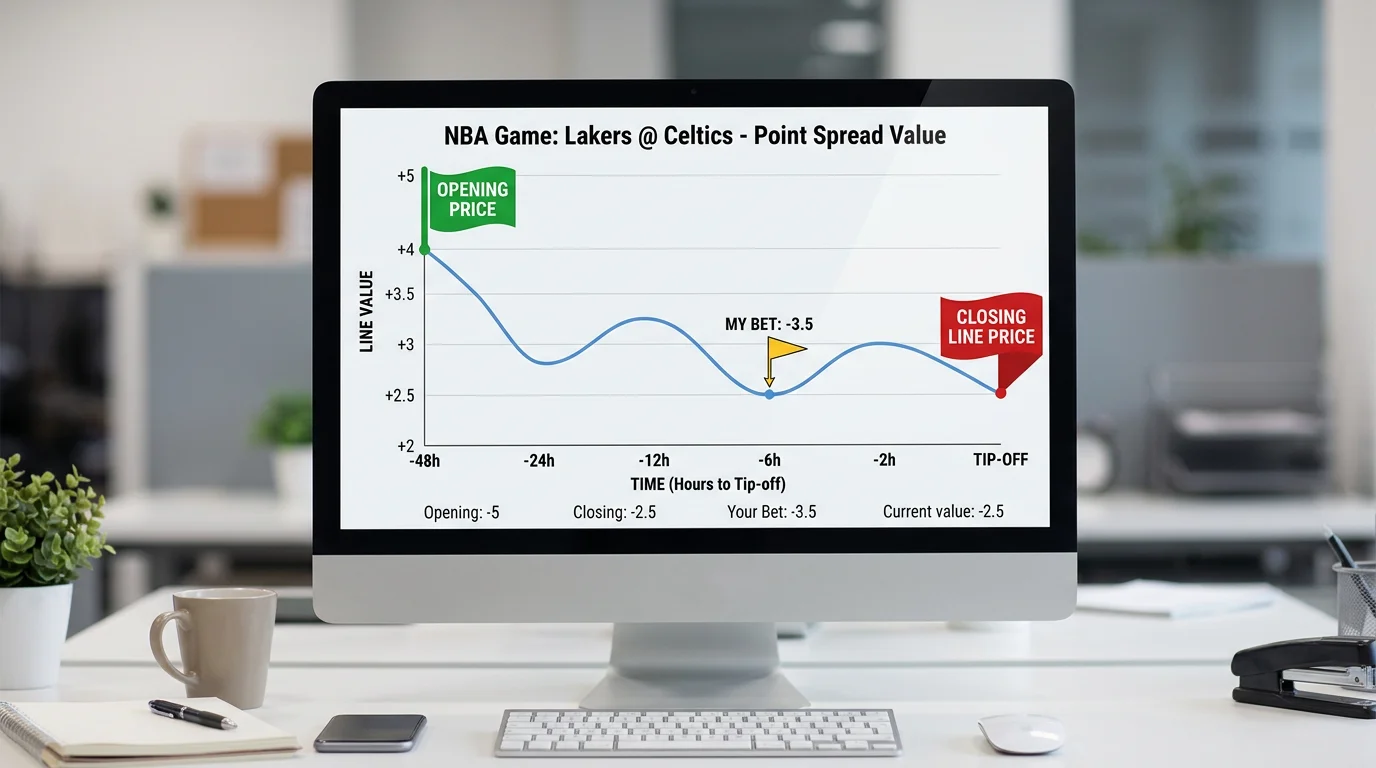

NBA spreads open the night before games at most UK books and immediately move as sharper money hits them. The opening number is not the consensus number – it is the book’s first guess, often produced by an automated model with limited information. If you have a process that beats that automated model, the first 30 minutes after a market opens is where your CLV will be highest.

This is genuinely hard to do in the UK because the markets open at unfriendly hours – late afternoon Eastern, which is late evening for us, often just as you are trying to wind down. But the edge here is real. A bet placed at +4 that closes at +2.5 has a point and a half of CLV, which in spread terms is enormous.

The trade-off: opening markets have lower limits. You will not be able to stake your normal amount on every open you want to hit. That is fine. The point is to capture CLV, build a record of doing so, and use that record to validate your process. Position sizing follows the validation, not the other way round.

The trap of confusing line movement with CLV

Line movement and closing line value are related but not identical, and conflating them is the most common mistake I see in betting content. CLV is specifically about where the line ends. A line can move three points across the day and still close at the same number it opened at. In that case, anyone who got the open had no CLV – the line went away from them and came back.

What you want is movement that holds. If you took the open and the line moved against you and stayed there until tip-off, you have CLV. If you took the open, the line moved your way, and then moved back, you have no CLV but you might have had a window to hedge or trade.

Some bettors trade rather than hold. They bet the early move expecting it to extend, then bet the other side later to lock in a small guaranteed profit. This is a different game with different mathematics. If you are doing it, your CLV measurement on the original bet is irrelevant – measure your net position instead. For UK bettors holding bets to settlement, traditional CLV is the right metric.

Markets where CLV is most reliable

Major NBA spreads and totals are where the closing line is sharpest and most predictive. Moneylines on heavy favourites can have weird CLV behaviour because the prices are compressed – going from -350 to -380 is a CLV move but feels insignificant. First-half markets and team totals are sharper than they used to be but still less efficient than full-game spreads.

Player props are the messiest CLV environment. Books do not always meaningfully update prop lines after the open, especially on lower-volume markets. A player rebounds line might open at 7.5 and close at 7.5 with no movement, but that does not mean it was efficient – it might mean nobody bet enough on it to move it. CLV measurement on props is less reliable as a result, and a lot of the work on those markets goes into building the kind of bottom-up projection process described in my notes on building a UK-friendly prop model from scratch.

What CLV cannot tell you

CLV is a measure of process quality, not outcome certainty. A bettor with strong CLV over 50 bets can still be in a losing stretch. A bettor with weak CLV over 50 bets can be in a winning stretch. Variance dominates short samples. CLV signals the underlying process is correct or incorrect – it does not predict the next week’s results.

It also cannot tell you about bankroll management, mental discipline, or whether you should be betting at all. You can have great CLV and still go broke through poor staking. You can have great CLV and still be making yourself miserable. The metric measures one specific thing – process edge against the market – and is silent on everything else that matters to being a healthy bettor.

UK gambling industry gross gaming yield was 15.6 billion pounds in the year ending March 2025, up 7.7 percent. A meaningful share of that growth came from people who win occasionally, feel good, bet more, and lose it back over time. CLV is the discipline that breaks that cycle, but only if you are honest with the numbers it produces.

The honest accounting that changed my approach

The first time I ran a full CLV analysis on my own betting, I sat with the result for a week before doing anything about it. The numbers said I was a slightly losing bettor pretending to be a slightly winning one. That hurt more than any individual losing bet ever did, because it meant the thing I thought I was good at I was actually mediocre at.

What followed was a six-month rebuild of my entire process. I cut the markets where my CLV was negative. I doubled down on the markets where it was positive. I changed how I scheduled my betting – earlier, more selective, more aligned with when the market was beatable. My win rate did not change dramatically. My CLV did, and a year later the bankroll caught up. That is the entire case for treating closing line value as the central metric of a serious NBA betting operation. Win rate tells you what just happened. CLV tells you what will happen, given enough time.

What is a good closing line value for NBA bets?

For spreads and totals, averaging half a point of CLV across your bets is meaningful, and a full point is excellent. For moneylines, look at the price differential – anything that implies you got 2 percent better than fair value is a real edge.

How do I track CLV if my UK bookmaker does not show closing lines?

Screenshot the line at tip-off yourself, or use a line-history service that captures market movements across multiple books. Recording the close manually is more work but free, and it makes you pay attention to the market.

Can a bettor with negative CLV still be profitable?

In small samples, yes – variance can mask process errors for months or even a season. Over hundreds of bets, negative CLV converges to negative ROI. Win rate eventually catches up with the underlying edge or lack of it.

Elaborado por el equipo de «nba bet of the day».