NBA Expected Value Betting in the UK: Finding +EV in Decimal Odds

- Why most UK punters never actually count their edge

- The EV formula on decimal odds, without the maths-anxiety

- Removing the vig: what the fair line actually looks like

- Line shopping at UK bookies turns thin edges into real ones

- Closing line value: the only retrospective metric that matters

- Applying EV to the four big NBA market types

- Common EV traps I see UK punters fall into

- Live EV in-play: where the mispricings actually live

- Questions UK punters ask about NBA EV

- Where a UK punter actually gets ahead

Why most UK punters never actually count their edge

The first time I tried to explain expected value to a mate over a pint, he stopped me halfway through and said, «So you’re telling me I’ve been betting for ten years without knowing whether any of it was a good idea?» That is roughly correct, yes. And he is in good company — most of the punters I have worked with over a decade of analysing NBA markets had never put a number next to the word «value», even when they used it constantly.

Here is the uncomfortable maths waiting at the start of every UK NBA bet. The average hold across regulated sportsbooks sits at 10.15%, meaning out of every £100 staked across the market, just over a tenner stays with the book. That is the headwind. You cannot beat it by feel, by hot takes, or by the comforting story that you «follow the games closely». You beat it — or at least, you stop bleeding to it — by being able to translate decimal odds into a probability, compare that probability to your own estimate, and only fire when the gap goes your way.

That is expected value. Strip away the jargon and EV is just a unit-of-stake-per-bet calculation: if I make this exact wager many times over, what is the average profit or loss? Positive number, you have an edge. Negative number, you are paying the book. Zero, you are gambling for entertainment, and that is fine — but call it what it is.

This guide is the version I wish someone had handed me at the start. We will walk through the formula on decimal odds (the UK default), strip the vig out of a market to find the fair line, look at how line shopping across UK books turns a tiny edge into a real one, and finish with where +EV hides in the live market when you are awake at 3 am watching a Lakers tip-off.

The EV formula on decimal odds, without the maths-anxiety

I will give you the formula first, then we will undress it. For a single back bet at decimal odds O, your true probability of winning p, and a one-unit stake, the expected value per unit staked is:

EV = (p x (O - 1)) - ((1 - p) x 1)

That is it. The first half is «how much I win, weighted by how often I win». The second half is «how much I lose, weighted by how often I lose». Add them and you have your average outcome per quid.

Worked example. The Celtics are 1.91 to win outright at a UK book. You have done the work and reckon they win 56% of the time. Plug in: EV = (0.56 x 0.91) - (0.44 x 1) = 0.5096 - 0.44 = 0.0696. Roughly 7p of expected profit on every £1 staked. Not life-changing on one bet. Life-changing on five hundred bets at the same edge.

Flip the example. Same price, but your honest probability is 48%. EV = (0.48 x 0.91) - (0.52 x 1) = 0.4368 - 0.52 = -0.0832. You are losing 8.3p per pound. The price did not change. Your read on the matchup did. EV is brutally honest in that way — it forces you to commit to a number for your probability, and the moment you do, the maths tells you whether to bet.

The thing nobody wants to admit is that the hard part is not the formula. It is the p. Where does your probability estimate actually come from? If the answer is «vibes», the formula is decorative. If the answer is a model — even a basic one — based on net rating, pace-adjusted points per possession, rest, and injury status, you have something to test. And testing is what separates +EV punters from people who say they bet +EV.

One practical note for UK punters: decimal odds make this maths a lot cleaner than the American format. American +110 is just 2.10 in decimal, but to compute EV from +110 directly you need extra conversion steps. Decimal is plug-and-play. This is one of the small structural advantages of betting in the UK that almost nobody talks about.

Removing the vig: what the fair line actually looks like

Now we get to the part where most «EV calculators» on the internet skip a step and let you down. Before you compare your probability to a bookmaker’s implied probability, you have to remove the bookmaker’s margin from their prices. Otherwise you are comparing apples to a slightly poisoned apple.

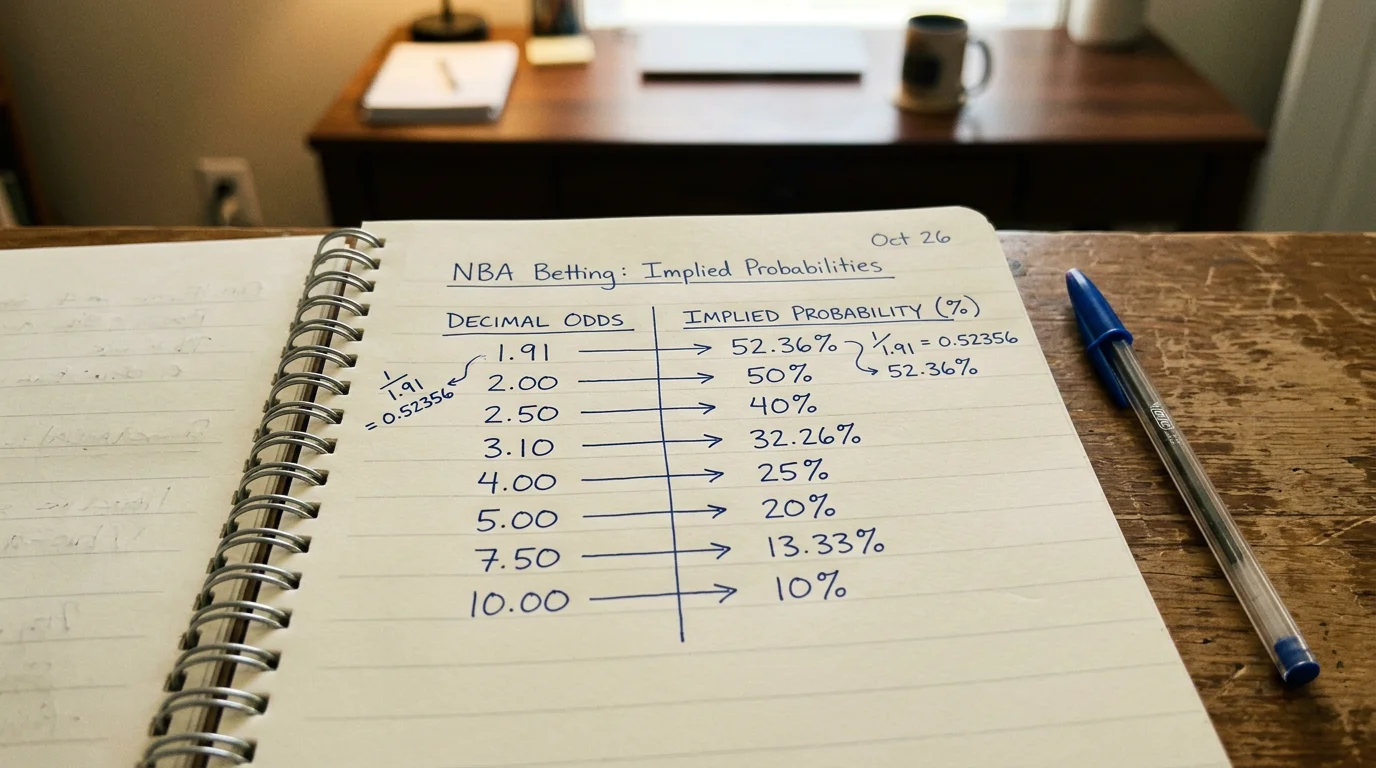

Here is the principle. A fair two-way market — say, a moneyline with no overround — would have the two decimal-odds-implied probabilities sum to 100%. Real bookmakers price markets so the two probabilities sum to something like 104% or 105%. That extra 4-5% is the vig, the juice, the hold. On average across regulated US sportsbooks the figure has been pegged at 10.15% for 2025, and UK NBA mainlines run comparably tight on moneylines, looser on totals and looser still on player props.

The de-vig procedure works like this. Take both decimal prices on a two-way market. Convert each to implied probability with 1 / O. Add them — you will get a number above 1.0. Divide each probability by that sum. Now they add to 1.0 and you have the no-vig fair probability for each side. Compare your model probability to that fair number, not the raw implied number, to assess true edge.

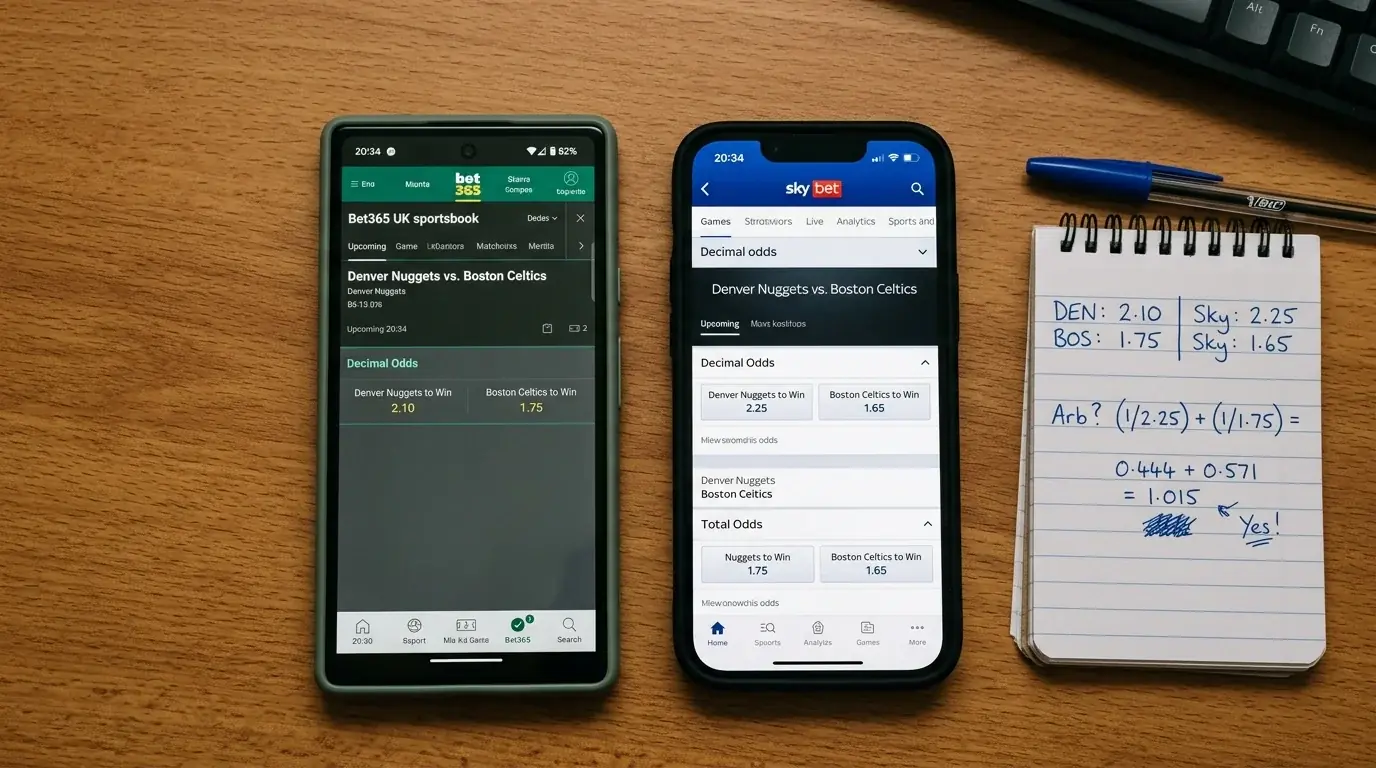

Worked example on an NBA moneyline. Suns 2.10, Nuggets 1.80. Raw implied: 0.4762 and 0.5556. Sum: 1.0318 (so the book holds about 3.1%, which is sharp for a UK NBA mainline). De-vigged: 0.4762 / 1.0318 = 0.4615 for Suns; 0.5556 / 1.0318 = 0.5385 for Nuggets. Now you have the bookmaker’s honest opinion. If your model says Suns win 49% of the time, you have a 2.85-percentage-point edge over the no-vig line. That is a real edge.

The same logic applies anywhere odds are quoted, but the margin you are pulling out gets nastier in some places than others. Parlay holds run as high as 24.2%, against just 4.4% on single bets. That is a structural disadvantage of 20 percentage points before you even pick a side. The de-vig procedure on a six-leg same game parlay returns a number so far from the offered price that the typical recreational SGP is mathematically indefensible. We will come back to that in the markets section, but file it away now: the bigger the parlay, the more vig you are paying, and no amount of clever leg selection rescues you from a 24% hold over a long enough run.

One more practical wrinkle. UK player-prop markets are often offered with a vig that pushes total implied probability past 110%. That is the bookmaker telling you, in maths, that they think their pricing is less precise than their moneyline pricing. Sometimes that imprecision works in your favour — those are the props worth hunting. Often it does not, and the cushion they have built in eats your edge. Either way, you should know the number before you click.

Line shopping at UK bookies turns thin edges into real ones

The fastest way to add EV to your bets, without improving your handicapping at all, is to hold accounts at multiple UKGC-licensed bookmakers and bet the best price on every selection. This is not a trick or a loophole. It is structural. Different books price the same game differently, and the gap between the best price and the median price on an NBA mainline is routinely 2-3 percentage points of implied probability. Across a season of NBA betting, that is the difference between flat and profitable.

The UK market makes this easier than the US market. Flutter Entertainment, which runs Sky Bet, Paddy Power, and Betfair under one corporate roof, posted group revenue of $15.91 billion for 2025, up 17% year on year. Entain, the parent of Ladbrokes and Coral, reported £5.3 billion in net gaming revenue with online UK and Ireland volume up 15%. Beyond those giants you have bet365, William Hill, BetVictor, Betfred, and a long tail of smaller licensed operators. Each prices independently. Each runs different promotions. Each has different exposure to the previous bettors who came through their doors that week.

What you are actually looking for in line shopping is two things. First, the best back-side price on a selection you already want. Second, situations where a single book has moved off the consensus line in a way you can exploit. The second is rarer than the first but pays better when it shows up. If five UK books have Lakers -4 and one has them at -3.5, you know the -3.5 is the line you want, and you do not need to think about it too hard.

The mechanics for the UK punter are simple enough. Open accounts at four or five licensed books. Use whichever odds-comparison habit you prefer — manually flicking between apps works fine if you do not bet huge volume. Place at the best price. Keep records. Notice patterns: which books reliably price a touch high on home favourites, which run sharper totals, which post props earlier and softer. The patterns are real and they are stable for months at a time before lines tighten.

The one thing to be sensible about is account longevity. Sharp UK punters who consistently take the best of the line will see stake limits arrive sooner rather than later, especially at recreational-skewed books. That is a fact of the industry, not a regulatory issue, and there is no clever way around it beyond rotating accounts and accepting that line shopping has a shelf life at any given operator. If you want to dive deeper into the specific tactics of pricing variance across UK books, I have a separate piece on how a half-point across bookies becomes real money.

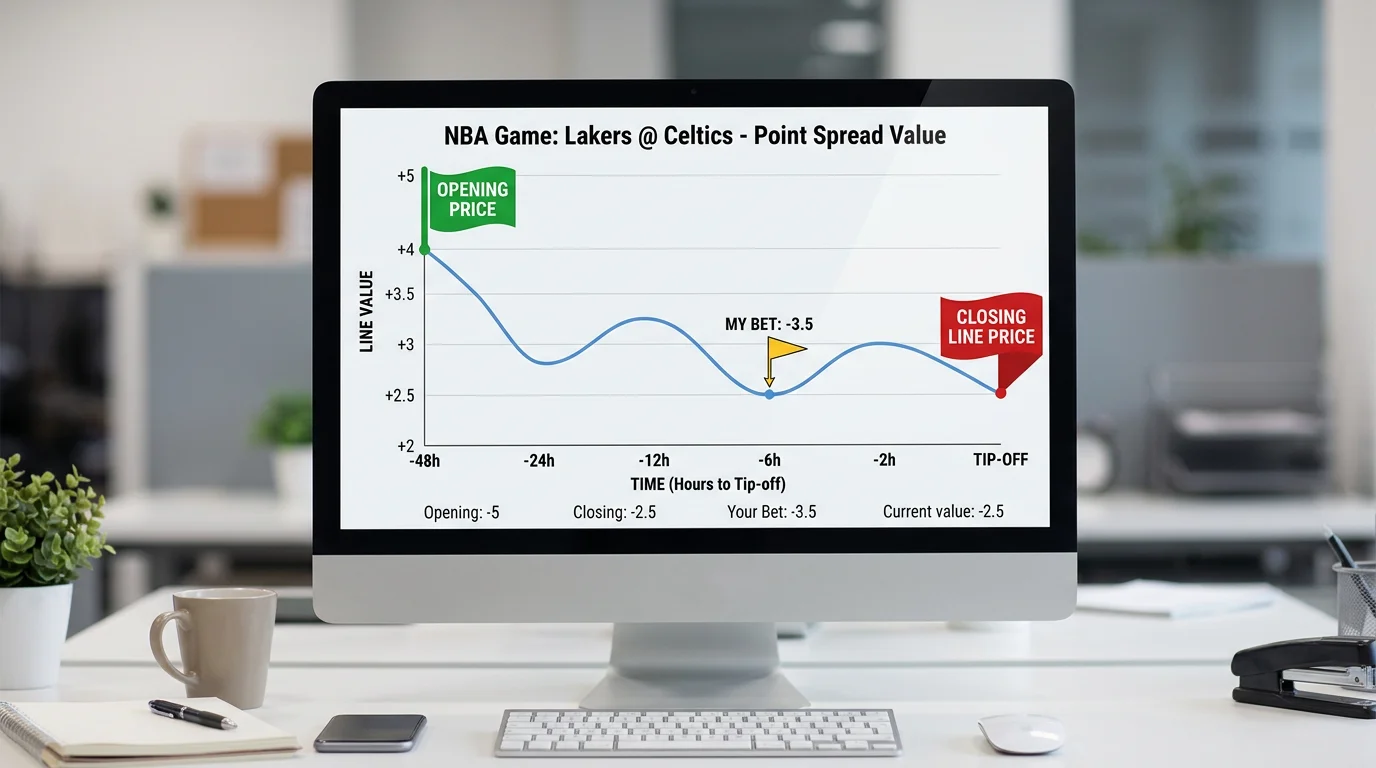

Closing line value: the only retrospective metric that matters

If EV is the prospective question — should I make this bet? — then closing line value is the retrospective one. Did I beat the market?

CLV is straightforward in principle. The closing line is the final price offered before tip-off, after the market has chewed on every piece of information and every sharp wager. Sportsbooks are not perfect, but the closing line is the most efficient version of their opinion. If you reliably bet selections at prices better than the closing line — say, you take the Suns at 2.10 and the line closes at 2.00 — you are systematically getting better prices than the market thinks are fair, and over thousands of bets that translates into profit.

The reason CLV matters more than win-rate for evaluating yourself is that win-rate is dominated by variance over reasonable sample sizes. A punter going 51% on point spreads at standard juice is profitable, but they will spend long stretches looking like they are losing even when they are doing everything right. CLV cuts through that. If your average CLV is positive, you are a winning bettor. If it is zero, you are running flat. If it is negative, the market is consistently moving away from your bets, and no amount of «I just had cold weeks» undoes that signal.

Tracking CLV in the UK requires a small amount of discipline. Record the decimal price at the moment you bet, and the closing decimal price at the same book. The difference, expressed as the implied-probability gap, is your CLV on that bet. Average it across a season. If the number is north of 1-1.5 percentage points, you have an edge worth scaling. If it is below zero, you have a problem and you need to find it, not bet through it.

One caveat I want to be honest about. CLV is a strong signal but not a perfect one. It is possible to grind out positive CLV on NBA props that are too thin to bet meaningful stakes on, while running flat or negative on the big markets where you actually put real money. Always look at CLV by market type, not as one blended number. Mainline CLV is what pays the bills. Prop CLV is what tells you whether your projections are sharper than the book.

Applying EV to the four big NBA market types

The general EV principle is universal. The way it shows up in practice differs sharply across NBA markets, and which markets you should hunt depends on where your edge is.

Moneyline. The simplest two-way market. Vig is typically the tightest of any NBA bet — around 3-5% in UK books on a competitive game. Edges are correspondingly small, often in the 1-3 percentage point range when they exist. Most recreational punters cannot reliably outperform the closing moneyline because the market on this market is mature and the public money is reasonably well-distributed between favourites and underdogs. The edges live in slow-news days, lookahead spots, and back-to-backs where the public underweights fatigue.

Point spread. The two-way handicap market. Slightly looser vig than moneyline, usually 4-5%. Edges here come from understanding where the spread is «wrong» relative to a model — most often around home-court advantage assumptions, which we now know have eroded sharply over the last 40 years. The closing-line home spread averages 2.05-2.10 points across recent seasons, with home teams covering the spread at just 50.1% — meaning the market has already priced in most of the HCA decline, but not all of it on specific matchups.

Totals. Over/under on combined points. Vig wider than spreads (5-7%), and pricing more dependent on pace, three-point variance, and rest. The 2025-26 season is averaging 101.9 possessions per 48 minutes, the highest pace in 30 years of play-by-play data, and 117.7 points per team — the third-highest in NBA history. That information is not secret. UK books know it. The edge is not «totals are higher now». The edge is identifying which specific games will pace below or above the expected number, and which prices have lagged the league-wide drift.

Player props. Where the vig spikes and where the projection work matters most. Live in-play markets, which include a growing share of prop volume, represent roughly half of all sports-betting handle in mature US markets, and the UK is trending the same way. Yahoo Sports’ parlay analyst summed up the trap concisely: «The mistake most bettors make with prop parlays is stacking too many legs. A 6-leg same-game parlay might pay +2500, but the probability of all 6 hitting is low enough that the expected value is usually negative.» That diagnosis applies just as cleanly to single-leg props bet without a projection: if you cannot estimate the player’s probability of going over the line within 2-3 percentage points, you cannot reliably find +EV against a vig that often exceeds 8%.

Common EV traps I see UK punters fall into

The first trap is treating bookmaker promotions as positive EV without doing the maths. «Bet £10, get £30 in free bets» sounds like a no-brainer. The actual cash-equivalent value of a £30 free bet at a UK book is typically around £20-22 — that is, free bets are «stake not returned», so a £30 free bet at evens returns £30 in winnings, not £60. The cash conversion rate depends on the price you place it at and your strategy. The bonus is positive EV at the point of claiming, but the wagering requirements that often attach are designed to suck back a chunk of that value, and the more you bet to «use» the bonus, the more vig you pay through the system. Free bets are not nothing, but they are not the headline number on the banner either.

The second trap is parlay maths. Combining four legs that you each believe to be +EV at 1.91 each does not give you a 12.3 fair line — it gives you a parlay that the bookmaker holds at 24%-plus on average. The hold scales viciously with leg count because each leg multiplies the vig. Two-leg parlay vig stacks. Three-leg vig stacks again. By six legs you are betting into a market where the book’s edge is so large that even genuinely sharp leg-by-leg selections cannot beat the combined drag. The disconnect between perceived value and actual value on parlays is where recreational money disappears.

The third trap is confusing «the book is offering a great price» with «this is a great bet». Sometimes the book is offering a great price because they have information you do not — a key player downgrade has not hit Twitter yet, a sharp move is brewing, the referee assignment shifts the totals expectation. If a price seems too generous relative to where you think the line should be, your first question should be «what do they know that I do not?» not «let me get this in before they move it». The market is not stupid and is rarely sleeping. Edges exist, but they are usually small and they look small. The five-percentage-point freebie almost always has a reason.

The fourth, which I see more in newer UK punters who have read a few US strategy posts, is over-rotating on +EV chasing at the cost of bankroll management. EV is the average expected outcome. Variance around that average is enormous. A bettor with a real 2% edge can still go 40 bets without a winning streak. If your bet sizing assumes the average outcome will hit close to the average over short stretches, you will go broke before your edge plays out. Kelly fractions, flat staking, percentage-of-bankroll discipline — these are not optional accessories to an EV strategy. They are part of it.

Live EV in-play: where the mispricings actually live

Live NBA betting in the UK has become its own beast, and the EV mathematics is meaningfully different from pre-match. Live markets make up roughly half of all sports-betting handle in mature markets, and the UK is trending hard in that direction. NBA games, with their natural quarter breaks and constant pace, are particularly well-suited to in-play, and UK books offer dense in-play markets — quarter winners, next-team-to-score, race-to-N-points, live spread and total adjustments.

The mispricings show up in a few predictable spots. Late first quarter, after a hot or cold shooting start, is when totals lines tend to over-react to small samples. A team that opens 6-of-8 from three is not a 60% three-point shooting team for the next three quarters, but the in-play total often moves as if they might be. The fade is mechanical: if the live total has jumped six points on the back of a high-variance early shooting performance, the regression bet on the under for the rest of the game is usually +EV.

The other spot is the late-game vig spike. With six minutes left and a five-point lead, the spread market widens its vig dramatically because the book is hedging against the volatility of a single fourth-quarter possession. If you have a strong read on a coach’s late-game tendencies — when they pull starters, how aggressive they are with timeouts, whether the trailing team plays fouls — you can occasionally find edges, but you are paying premium vig for them. The maths on whether that vig is worth paying is rarely flattering.

The trap in live EV is latency. UK punters are usually watching on a Prime Video or Sky stream with at least a few seconds of delay against the actual game feed, and books are pricing against syndicated data with their own delays. The window in which a true mispricing exists is small, and the moment you click, the book may have already moved or suspended the market. Live EV is real, but it is a faster game than pre-match, and it rewards punters who can model quickly and accept that some of their best clicks will be rejected by the book pulling the price first.

Questions UK punters ask about NBA EV

How do I calculate expected value from decimal odds offered by UK bookmakers?

Use the formula EV = (p x (O – 1)) – ((1 – p) x 1), where O is the decimal price and p is your estimated probability of winning. A 1.91 price needs you to win more than 52.4% of the time to break even before vig, and your edge is anything above that threshold. The hard part is not the formula but committing to an honest probability estimate, ideally from a model rather than a feel.

Is closing line value a reliable proxy for long-term NBA profit?

Yes, more reliable than win-rate over the sample sizes most UK punters accumulate in a season. CLV measures whether you systematically beat the market price at the moment the line closes — if your average CLV is positive across hundreds of bets, you are likely a winning bettor even if short-term results say otherwise. Track CLV by market type, since mainline CLV behaves differently from prop CLV.

Do live NBA markets offer more +EV than pre-match lines?

Sometimes, but the edge is harder to capture cleanly. Live markets carry wider vig, especially in the late game, and feed latency between your screen and the bookmaker’s pricing engine eats into reaction time. The best live +EV usually comes from regression spots — totals over-reacting to small-sample hot or cold shooting — rather than from quarter-by-quarter directional bets.

Where a UK punter actually gets ahead

EV is not a magic word. It is a discipline. It says: do not bet unless you can justify the wager with a number, not a feeling. The number does not have to be precise to four decimal places — your model can be rough, your probability estimate can carry honest uncertainty — but the discipline of writing it down, comparing it to the no-vig fair line, and only firing on the gaps that favour you is what separates breakeven punters from losing punters and, eventually, separates winning punters from breakeven ones.

The UK market is not a hostile environment for this. Decimal odds make the maths clean. Multiple licensed operators make line shopping possible. The growing volume of live and prop markets creates more shots on goal for punters willing to do the projection work. The 10.15% average hold across the broader industry is the hill you climb, but it is a climb that the maths can win — provided you stop treating EV as a piece of jargon and start treating it as the only question that matters before clicking «place bet».

Creado por la redacción de «nba bet of the day».